7 Days 7 Lessons #11

- Lesson 1: Life Razor (Mindset)

- Lesson 2: Allegory of the Ring (Morality)

- Lesson 3: How To Allocate Your Extra Money (Growth)

- Lesson 4: The 3 Stages of the Stock Market (Finance)

- Lesson 5: Focus On Your Relationships (Relationships)

- Lesson 6: How To Tell A Story (Soft-Skill)

- Lesson 7: ISAs: A Tax Efficient Way to Earn Passive Income (Finance)

Hope you're having a fantastic week!

Keep your heads high and locked on your dream!

Life Razor

One statement that will help you answer any question.

You've been offered your dream job, with an incredible salary; however, it comes with the condition that you move to a different country. Would you take it?

There are so many things to consider if this were to ever happen to you. For example:

- Do I have a family? Would they be willing to relocate? Would it be good for them to relocate?

- How much more money is it? Can I get this job in the city I'm in right now?

- Do I want to live in the new country?

- Do I have friends there? How lonely will I feel?

This one question would very quickly overwhelm you. There's just so much to think about it, and it could mean you make the wrong decision.

In his book, The 5 Types of Wealth, Sahil Bloom offers one simple statement that anyone can build to help you answer any question.

The Life Razor is a one-sentence statement defining your identity. Your identity statement should be:

- Controllable – You must be able to achieve your identity.

- Beneficial – Does this identity benefit the rest of the areas in your life?

- Identity Defining – It should describe to the world the type of person you are.

This is mine:

I am a devote Christian. I want to live a good life, one where I fufill what I was meant to do. I want to love and care for everyone I come across, especially my friends, family, future kids, and soon-to-be wife. I want to follow in Jesus Christ's footsteps. – I am a Man of God.

With this statement, I can answer any question, including the hypothetical above.

As a Man of God, I would not do anything that would sacrifice the relationships I have and the ability to love those around me. I would not jeopardise my family, nor would I take a job if it comes with immoral work. Money is not the be-all and end-all, and I would also be willing to sacrifice my dreams if it meant I could be a better Man of God.

With the above statement, I can now compare it to the job offer I received. If the job offer at any point infringes on my mission statement, then the answer is clear. No. But if it doesn't, it's also clear. It's a Yes.

Life Razor, a simple mission statement, an identity-defining statement, a stand-your-ground statement, that has made decision-making so much easier for me, and I can guarantee it will make it easier for you.

Don't like drinking? So why on earth would you go to the club? Hate football? So why would you go to an Arsenal football match? Don't like playing video games? So why would you buy the new Call of Duty?

Our identity can be used to answer questions quickly and easily. If you have a choice to make, ask yourself: What would the person I claim to be choose in this situation?

TLDR: Define who you are, and then use that identity-defining statement to help make life decisions.

Allegory of the Ring

Is morality objective or subjective?

The Allegory of the Ring starts with Gyges discovering a magical ring that makes him invisible. Gyges then used this ring to sneak into the royal palace, seduce the queen, kill the king and seize the throne.

This story was told through Glaucon, and he claims that a just man and an unjust man would both use the ring identically, in a way that fulfils their personal desires. He claims that people behave justly because of fear of punishment or to seek reputation, not because justice means anything.

Honestly, I disagree with this claim. Imagine you have this ring. Now imagine some of the most heinous things you could do in your life. Now imagine that a condition was met where committing that heinous crime wouldn't be revealed. Would you feel bad when doing it? I would argue that any sane person would.

Let's take the example Glaucon presents with Gyges. You deeply fancy the queen of your land. But the only problem is, she has a husband. A quick way of fixing this is by murdering the husband and substituting yourself for him. Not only have you achieved a beautiful queen, but also wealth and power. Three things that most people would desire.

Would you do this? Could you force yourself to kill someone, even if there were no repercussions, and even if no one would know you did it? Could you see the life leave someone's body, and because no one saw it, you'd claim it was fine.

I don't think any non-psychopathic person could do this. There is something deeply intrinsic in our bodies that prevents us from carrying out certain malicious acts. We might call it common law, but I call it objective morality. Although commonly disputed nowadays, I think this story is a perfect example that objective morality does exist.

You could argue that not carrying out immoral activities is caused by deep social conditioning, empathy or evolved instincts, not objective morality, and I would say you make a fair point. If that was the only evidence I presented to you, I wouldn't expect you to change your mind, but the more you go down the rabbit hole, the more I think it sides with objective morality.

As a Christian, I believe in objective morality. I believe in right and wrong. I don't believe that we happened to come across a set of laws law that people around the world would agree on. We don't even agree on the simplest of things. You think a law book that prevents heinous, self-indulging crimes would be agreed upon?

The Allegory of the Ring is a perfect story that sheds some light on the battle between objective and subjective morality. I wonder what you think.

TLDR: The Allegory of the Ring begs the question of whether justice is carried out for fear of repercussion and reputational gain or whether it is something inscribed within our hearts.

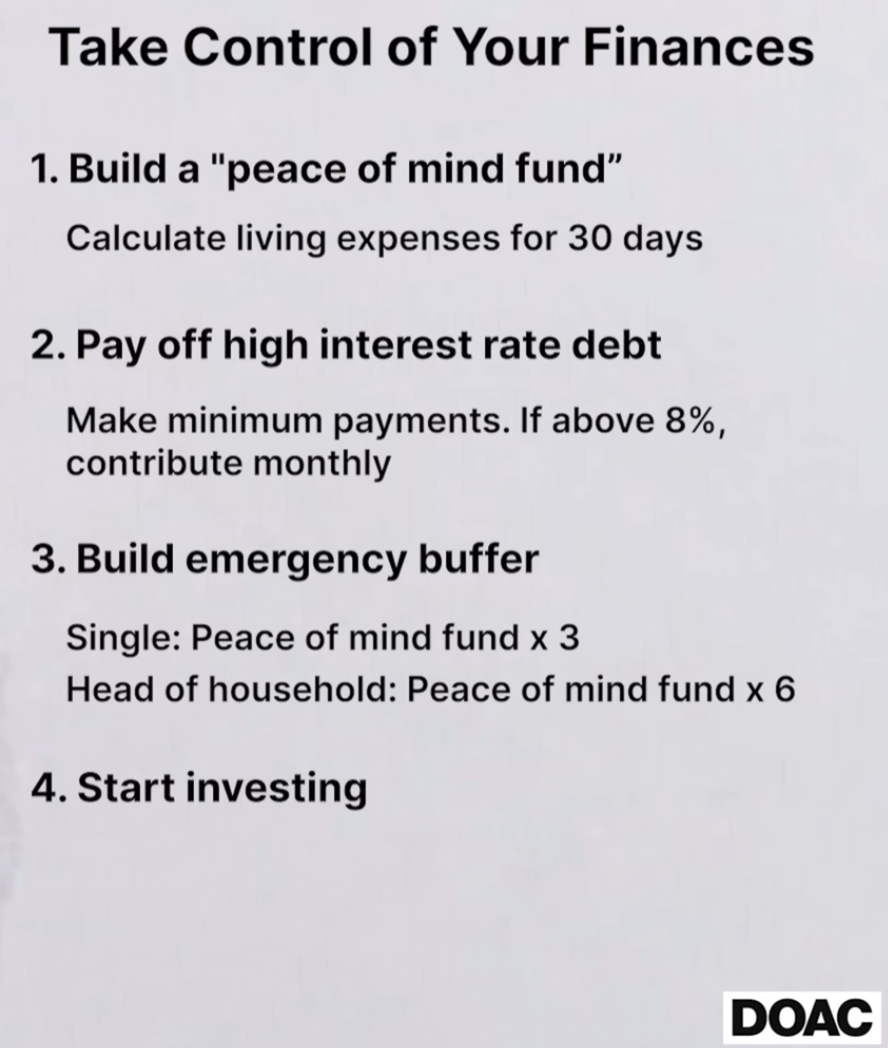

How To Allocate Your Extra Money

Four simple steps to ensure you're putting your extra money in the right places.

You've started your first job, or you simply want to become more financially smart. Where should you put your extra money?

Nischa Shah and JL Collins, two experts in personal finance, recommend the following strategy.

- Create a peace of mind fund – Look at how much you've spent in the past month. Make sure you cover that in your savings. 47% of Americans can't pay a £1,000 emergency bill, and 30% of UK citizens can't cover 1 month of living expenses. Give yourself breathing room in your financial life.

- Pay off high-interest-rate debt – High-interest debt eats away at your cash flow. Get rid of it as quickly as possible. You can even use credit cards for this. Let's say, for example, you have a loan at an interest rate of 30%, but your credit card is at 20%. Covering your loan with your credit card means you save 10% on future interest payments. Don't go crazy with credit cards; you don't want to create a new problem. Cover the holes in your sinking ship!

- Emergency Fund – Create an emergency fund of 3-6 months of monthly expenses. This gives you flexibility in life, which is a great way of making you much happier. You become less scared of losing your job or a massive bill coming your way. Saving 3-6 months of expenses does more to your wellbeing that earning 200k. Only save money for certain goals; otherwise, move it to step 4.

- Put your money to work - Saving until retirement is a bad idea. Putting it into a savings account at best beats inflation by 1%, but in most cases loses you money against inflation. That's why it's a good idea to put it to work. Look at buying bonds, stocks, and other forms of investments. Consider investing in your retirement account, too! Diversification is key to any portfolio.

These four simple steps are recommended by every personal finance expert I've read or watched. There's no surprise to it. It focuses on efficiency, freedom and peace of mind.

Achieving a higher and higher wage is definitely the best way of improving your financial position. But improving your financial efficiency will mean your money lasts longer.

Knowing exactly where to put your money in life is important to put your mind at ease and ensure that your money is doing the best it can for you.

TLDR: Firstly, create breathing room. Next, pay off high-interest debt. Thirdly, create even more breathing room. Lastly, put your money to work.

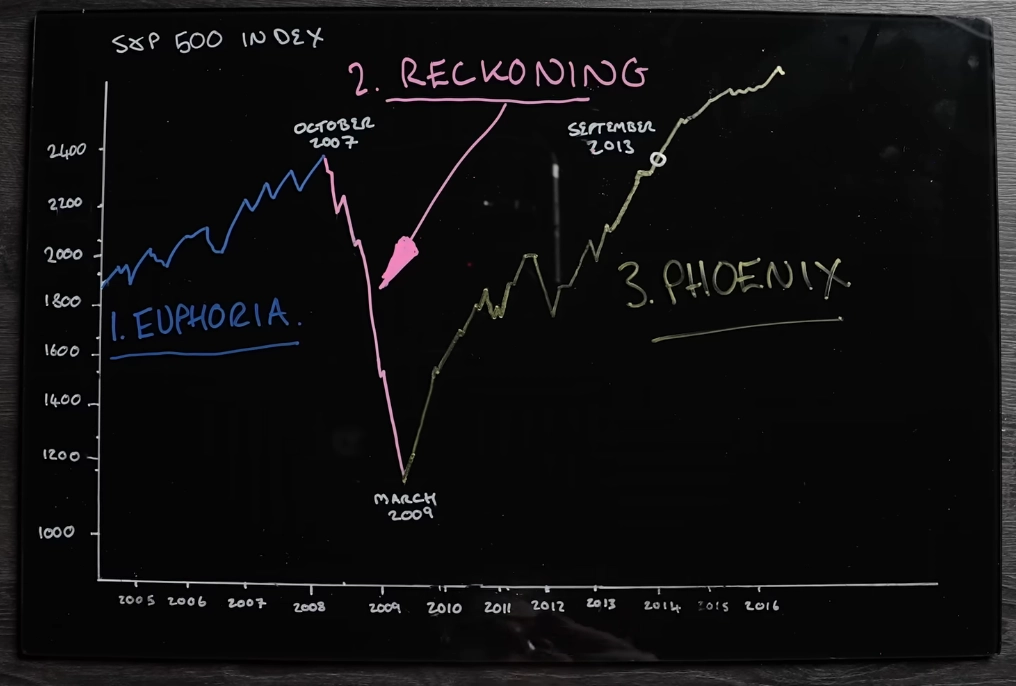

The 3 Stages of the Stock Market

One thing that history tells us is that the world always bounces back.

If you're starting to invest, the best thing you can do is get comfortable with the fact that the stock market will crash many times during the time you're invested in.

I've been investing for 5 years, and although that might not seem like a lot, I've been in quite a few stock market crashes so far.

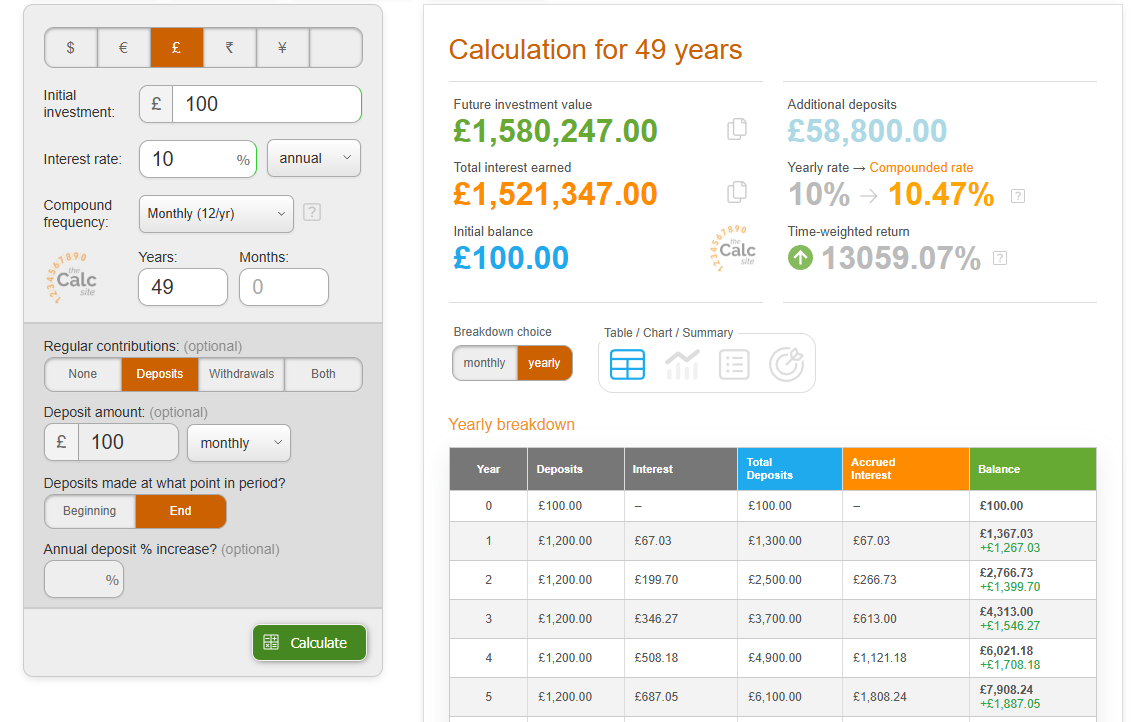

Imagine you're 67 years old, you've just entered retirement in the UK, and you started investing at the age of 18. You would have lived through 18 stock market crashes that consisted of the UK, Europe, the US, or the world.

Knowing that, it's important not to panic in these situations. If you had continued to buy the S&P 500 during the entire time you were investing, and never stopped, you would be sitting on more than £1.5 million.

To help you be more at peace, I wanted to introduce you to the 3 stages of the stock market, the idea that I found from Mark Tilbury.

- Stage 1: Euphoria – During this stage, there is a lot of hype in the market. Valuations are crazy or leaning heavily towards the future. There's a good chance a correction is coming. The best things to do are:

- Minimise your risk level – Maybe having 20% of your portfolio on Bitcoin isn't a great idea.

- Reduce any leverage you may have – If you've borrowed money to invest, I would recommend that you pay that back, as you could be margin called.

- Save extra cash – Make sure you have extra cash in the bank so you can continue to live life if half of your stock portfolio disappears. It also means you have the ability to buy extra stock at discounted prices.

- Diversify – Make sure you've got your money spread in many different assets. Not just one stock or one cryptocurrency. Crashes are where most companies go bankrupt, and you don't want your money to go with them.

- Stage 2: Reckoning – The crash has happened, the stock market has lost 10-80% of its value; however, if you've prepared, the stock market is on a black friday discount. The best things to do are:

- Remove any emotion – Don't let the price of stocks going down force you to sell a company that would eventually return to all-time highs. You chose your stock for a reason; that reason should still be good even if the stock market crashes.

- Continue buying stock – It's black friday, buy more stocks and decrease your overall buying price.

- Maximise your cash flow – Make more money. Recessions make people rich; take advantage of this wealth-building opportunity.

- Stage 3: Phoenix – This is calm after the storm. Just rake in the rewards by continuing to invest. Eventually, the peaks of the stock market will be reached again, and you will get your money and more back.

Recessions are horrible for those unprepared, but if you can capture the moment, you can turn a serious profit.

The stock market has never been stable. It's full of speculation, novice investors, investors with more knowledge than the outside world, is impacted by economic events, and is live to trade 5 days a week, 7 hours a day.

This all leads to fluctuations. This leads to emotional trading. This leads to mistakes. Do what all the best investors in the world recommend. Buy a low-cost ETF and invest the same amount every month. Do that during the highs, the lows, and the average.

TLDR: Stocks boom, and they crash. Continue investing during every stage of the cycle. One thing has been consistent: the stock market always recovers.

Focus On Your Relationships

Relationships are one of the most important foundations in your life.

In the summer of 2021, I moved away from the city I called home for 18 years to live 212 miles away in a city called Liverpool.

One thing I learned really quickly was that the real-world, the non-student life world, will consume most of our lives, and this is the last real time, before retirement, that I can spend a lot of time hanging out with my friends.

I realised this early because I was homesick. I missed my school friends, and although we did hang out here and there over the phone, it just wasn't the same as hanging out in person.

Unfortunately, people insisted on staying at home and not many in-person meetups happened. The ones that did I cherished deeply.

Eventually, the gig was up. A lot of us had finished university, and the real-world hit us. Some were working evening shifts. Some were still doing uni. Some were travelling and working. Some just didn't have time to hang out.

One thing was true. The opportunity to hang out with friends for hours and hours on end was put on an indefinite pause.

I learned this early because I moved so far away from everyone. I can't really do much with it now. But I want to emphasise this lesson to the people who still have time to spend 12 hours playing video games and chilling in the park doing silly things with their friends.

Eventually, the world is going to demand more of you, and eventually, you will lose a lot of the freedom you once had. Cherish it, and make the most out of it.

TLDR: The abundant free time you have when you're still a student will only continue to shrink when you get a job, get married, and have kids. Cherish the time you have when you're young to find your best mates, people who you want to see in your life consistently.

How To Tell A Story

A powerful tool that is used by every successful person in the world.

This week, as part of my training, I had a storytelling soft skills module I took part in.

Honestly, I thought it was good. Storytelling is an incredibly valuable skill to have. It helps you connect with people, and in a job where communicating with different stakeholders, all with their own wants and needs, is critical.

Storytelling helps...

- You appear more human.

- Communicate your perspective to others.

- Convey important messages.

- Build Relationships.

- Share understanding.

- Build hope.

- Build authenticity.

Below is a guide I was given on how to write a story.

- Beginning – Every story needs a start. Provide a time and a place, don't waffle and capture people's attention in the introduction.

- Middle – Use relevant details to explain what's happening. Name key people and use natural, conversational language.

- End – The bridge. What's the moral of the story you're trying to convey? Why did you tell the story?

I was also given a lot of good tips, such as:

- Describe the actions of a person, not their emotions – This is more powerful.

- Go deeper – be descriptive, help people visualise the story. But don't overdo it.

- Think bigger – what is the impact of you telling this story?

- Get personal – share your thoughts and feelings

- Solve a need – have the story make someones life better.

- Stories must be authentic and powerful.

Want to convince someone why they should choose your solution over someone else's? Tell a story. Want to captivate your audience in the first 5 minutes of a presentation? Tell a story.

Storytelling is such a powerful tool, and it's a shame people don't use it more often. In a world that is becoming increasingly divided and people strip the humanity away from others, storytelling is a way to fight back against this.

TLDR: Storytelling is a great way to get people to see who you are and share your perspective.

ISAs: A Tax Efficient Way to Earn Passive Income

As of 2026, the Capital Gains Tax Allowance is £3,000. Therefore, if you earned more than this from any of the above examples, you may be subject to tax ranging from 18%-32%.

Most people don't realise this and are hit with an unexpected tax bill.

Introducing Individual Savings Accounts (ISAs). These are tax-efficient savings or investment accounts that you can use to protect any profit you make.

Every tax year, you receive an allowance of £20,000. This means every year you can contribute a maximum of £20,000 to your tax-efficient account. Whilst in there, any money gained is tax-free!

There are 3 main types of ISAs, including:

- Cash ISAs – Essentially a tax-efficient savings account.

- Stocks and Shares ISAs – If you're interested in investing, this is the place to go. Any money earned is not taxed. That means you could make £1,000,000 in profit from investing, and that would not be taxed.

- Lifetime ISAs – These are for first-time home buyers or people planning on retiring. You can contribute every year up to £4,000. The government will contribute an extra 25% for every pound contributed.

Financial Interest provides an up-to-date list of all the best ISAs in the UK right now. What are you waiting for? Move your money into ISAs and pay no tax on what you make!

This shocking number just shows how common financial illiteracy is within the UK.

ISAs have almost no disadvantages and should always be used over a non-ISA account. They are no-brainers and incredible wealth-building tools that the government provides for you to avoid paying tax. Get yours today!

TLDR: The UK provides a legal way to avoid tax from owning and selling assets. Do you have one, and if you don't, why not?

Quotes Of The Week

- "Your failure here is a metaphor. To learn for what, please resume climbing." – Rob Dubbin

- "This thing we call 'failure' is not the falling down, but the staying down." – Mary Pickford

- "To live is to suffer, to survive is to find some meaning in the suffering." – Friedrich Nietzsche

- "Our doubts are traitors, and make us lose the good we oft might win, by fearing to attempt." – William Shakespeare